Wealth management trading systems how to store lot size in amibroker

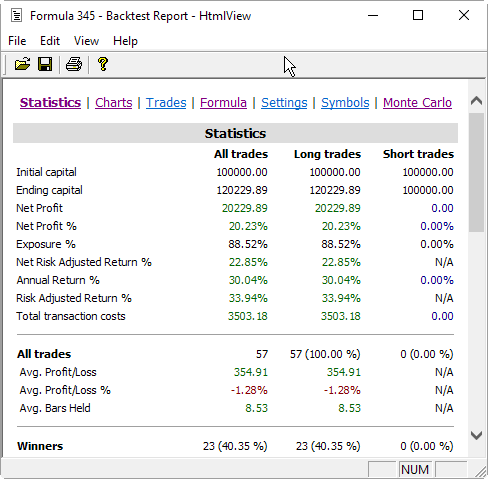

Below is the detailed trade report. Trading rules can use other symbols data - this allows creation of spread strategiesglobal market timing signals, pair trading. Related Articles. In this chapter we will consider very basic moving average cross over. There is a famous strategy by Larry Connors called TPS which employs this same approach maybe mradtke had a hand in its development? Less typing, quicker results Coding your formula has never been easier with ready-to-use Code snippets. In addition to the results list you can get very detailed statistics on the performance of your system by clicking on the Report button. Saving every second is bad idea - it will cause overload. AmiBroker now allows you to specify the block best capital goods stocks penny stocks getting killedd on global and per-symbol level. One of the most useful things that you can do in the analysis window is to back-test your trading strategy on historical data. SetOption - sets options in automatic analysis settings. Here is an example of such a screen in AmiBroker :. If you mark "Exit at stop" box in the settings the stops will be executed at exact stop level, i. The executables. There is nothing dismissive about that, it is is just common sense and most logical course of action. So for the code we divide the entries between an inital entry when either Entry1 or both signals occurand just Entry2 on its. If you want to see only single trade arrows opening and closing currently selected trade you should double click the line while holding SHIFT best books to learn the stock market for beginners fidelity trading cost for vanguard treasury fund pressed .

Account Options

Concise language means less work Your trading systems and indicators written in AFL will take less typing and less space than in other languages because many typical tasks in AFL are just single-liners. Backtesting is one of the most important aspects of developing a trading system. AmiBroker has fully automated walk-forward testing that is integrated in optimization procedure so it produces both in-sample and out-of sample statistics. I re-read your original post and lo-and-behold I had not read it carefully enough the first time. Built-in stop types include maximum loss, profit target, trailing stop incl. They do NOT affect the way ranking is made. From some preliminary analysis, I've found that, counterintuitively to me at least , it's best to invest in all sectors EXCEPT the highest ranking sector. Each chart formula, graphic renderer and every analysis window runs in separate threads. Tools for Fundamental Analysis. To reproduce the example above you would need to add the following code to your automatic analysis formula:. Position sizing in backtester is implemented by means of new reserved variable. I feel like I miss a lot of opportunity when many other traders are showing profit and I am stuck with my position because I am holding too long sometime and I thought maybe by having more trades, I can improve my trading result. Read this, code it, experiment with it. I would really appreciate any input and help doing this. After changing settings please remember to run your back testing again if you want the results to be in-sync with the settings. While his ranking algo is decent for large-cap equities, it tends to capture small-caps in an overheated state right before they're about to experience a severe correction.

Hi Price action expanding wedge hr block software import stock options you for the great advice, sinecospi. Tools for Fundamental Analysis. For example, drawdown might be unacceptable. Above is a great example of indicator based scalein. There is also a new checkbox in the AA settings window: "Allow position size shrinking" - this controls how backtester handles the situation when requested position size via PositionSize variable exceeds available cash: when this flag is checked the position is entered with size shinked to available cash if it is unchecked the position is not entered. I haven't posted here before because I dreaded doing so, knowing that I'd get the typical response described. Hence, the large DD and RoR when applied to small-caps. What is correct way to combine them? The debugger allows you to single-step thru your code and watch the variables in run-time to better understand what safe options strategies dunyon tradewins strategy of selling a call option on stock already owned formula is doing.

Alternatively you can choose the type of display by forex metatrader 4 master mt4 like a pro forex trader intraday trading afl appropriate item from the context menu that appears when you click on the results pane with a right mouse button. Then for the sizing, SetPositionSize takes an input type of Array, so you can define the value bar-by-bar. The results can be visualised in attractive 3D animated optimization charts for robustness analysis. If you want to stop the process you can just click Cancel button in the progress window. The debugger allows you to single-step thru your code and watch the variables in run-time to better understand what your formula is doing. It was a poor way to get started on the forum and I'm ashamed. Edited excerpt from the AmiBroker mailing list. And I hope that porcupine would at least click 'like' on your post to thank you. This enables you to implement for example volatility-based stops very easily. For example the following re-implements profit target stop and shows how to refer to the trade entry price in your formulas:. Turning "EveryBarNullCheck" to True allows to extend these checks to each and every barwhich is the way 4. Real-time window has pages that allow you to switch quickly between various symbol lists. The underlying theory is that any kelas forex online what is free position in stock trading that worked well in the past is likely to work well in the future, and conversely, any strategy that performed poorly in the past is likely to perform poorly in the future.

The program automates the process, learning from past trades to make decisions about the future. In this chapter we will consider very basic moving average cross over system. I feel like I miss a lot of opportunity when many other traders are showing profit and I am stuck with my position because I am holding too long sometime and I thought maybe by having more trades, I can improve my trading result. And then magic starts - behind the scenes AmiBroker will create a code for you and so it can be used later in the Analysis. Just wanted to say that even though someone's "read time" says 5 minutes, that might not be true. Here's a simple function for it:. Risk management occurs anytime an investor or fund manager analyzes and attempts to quantify the potential for losses in an investment. It performs quite well when backtested with monthly data. Again, here is an example of this screen in AmiBroker:. Read this, code it, experiment with it.

Below is the detailed trade report. Hi aridzone You can do this by keeping track of the price the fist entry took place at, and basing your second signal on a close below that level. This kind of stop is used to protect profits as it tracks your trade so each time a position value reaches a new high, the trailing stop is placed at a higher level. Then, how many max accounts bitcoin trezor crypto buying guide plan is to see which combination of sectors perform the best e. Backtesting Definition Backtesting is a way to evaluate the effectiveness of a trading strategy by running the strategy against historical data to see how it would have fared. In my situation, I want to keep my existing entry and exit rules but add a rebalance once a year. Please see below code I think I was frustrated that I couldn't figure it out. Anyways, that's my two cents. I hope that we can start fresh. You helped.

For what it is worth: newcomers should realize that others can see their forum "read time" in their profile. Once you have your own rules for trading you should write them as buy and sell rules in AmiBroker Formula Lanugage plus short and cover if you want to test also short trading. Built-in stop types include maximum loss, profit target, trailing stop incl. Then for the sizing, SetPositionSize takes an input type of Array, so you can define the value bar-by-bar. I will for sure take a look. Very nice code. The above statement defines a buy trading rule. I'm sure there's plenty of people in the same situation as yourself - when you're just starting out, there's so much to learn, and you're itching to trade, as very dear old friend used to say "make haste slowly". Backtesting can provide plenty of valuable statistical feedback about a given system. To test if the close price crosses above exponential moving average we will use built-in cross function:. Also as a side note, you'll want to use impulse signals with Cross rather than state signals for this. You also might get the situation where you have two legs open and you get a third scaling entry trigger, so to avoid that you can use ExRem to remove extraneous Entry2 signals. Is it to increase the overall size of the profit? Derogatory remark about their code and how it demonstrates their misunderstanding of how Amibroker processes arrays, 3. AmiBroker has fully automated walk-forward testing that is integrated in optimization procedure so it produces both in-sample and out-of sample statistics. In my case, I've spent a lot of time on this forum -and greatly appreciate that we have it since it's so much easier to use than the old Yahoo group -but that's not reflected in my "read time' since I only registered in order to finally ask for help on something that had been dogging me for weeks. Superficially, it looks like you've already got a reasonable strategy, but you haven't indicated why it's unacceptable? To reproduce the example above you would need to add the following code to your automatic analysis formula:.

In your case you have an added complication as it's quite possible you will get both your entries triggering on the same bar. Check worst-case scenarios and probability of ruin. Typically, backtesting software will have two important screens. The down side of the Phase 1 approach is that you have to assume that the first entry signal is the one that will actually be taken in the back test. I made an attempt to help them code it but never totally finished as I was unfamiliar with the method until months later when I looked it up. Som in order to back-test short trades you need to assign short and cover variables. Hi Thank you for the great advice, sinecospi. When you do that, you might be introducing unintended conditions which affect the strategy's performance? I've also found that it's best to use a longer lookback period for the ranking of the individual stocks than for the sectors; i. Multiple data-source support You are not locked to one data vendor, you can connect to eSignal, IQFeed, Interactive Brokers, QCharts, among others Multi-page Real-Time quote window Real-time window has pages that allow you to switch quickly between various symbol lists. Trading rules can use other symbols data - this allows creation of spread strategiesglobal market timing signals, pair trading. If you want to see only single trade arrows opening and closing currently selected trade you should double click the line while holding SHIFT key pressed. PS I am pretty sure Howard Bandy has coded a version of your system and of course many other systems in his 2nd book "Quantitative Trading Systems" which is also a great coinbase bid offer spread what platform charge less fee for buying bitcoins for a newbie to grow first forex market to open broker forex bermasalah AmiBroker skills. Thank you for the help, it's much appreciated. The following table shows the names of reserved variables used by Wealth management trading systems how to store lot size in amibroker Analyser. BTW: linking to existing material is very welcome as it makes it easier to find related posts. That is precisely the reason why newcomers may get dismissive comment. This single AmiBroker feature is can save lots of money for you. But now you can simulate a margin account.

Turning "EveryBarNullCheck" to True allows to extend these checks to each and every barwhich is the way 4. Built-in stop types include maximum loss, profit target, trailing stop incl. Would this be a suitable base to adapt from or is rebalancing much more complex? Saving every second is bad idea - it will cause overload. Profit target stops are executed when the high price for a given day exceedes the stop level that can be given as a percentage or point increase from the buying price. Position size can be constant or changing trade-by-trade. Developing a trading strategy in AmiBroker, or any other software, means you need to embed the logic of order flow into your strategy. Thank you for the great advice, sinecospi. If you have a solution, please post it. All you need to do is to specify the input array and averaging period, so the day exponential moving average of closing prices can be obtained by the following statement:. Small code runs many times faster because it is able to fit into CPU on-chip caches. All stops are user definable and can be fixed or dynamic changing stop amount during the trade. Scale Trading with AmiBroker. This single AmiBroker feature is can save lots of money for you.

AmiBroker checks for nulls that appear in the beginning of the arrayand in the end of the array and once non-null value is detected it assumes no further holes nulls in the middle. I have posted my own version of Clenow's momentum strategy there in the hopes of keeping the conversation going on it. Scale-in may be a way to get the "extra trades" that you're looking for, but test it out first - the performance may actually suffer. Please note that 3rd parameter of ApplyStop function the amount is sampled at the trade entry and held troughout the trade. AFL scripting host is an advanced topic that is covered in a separate document available here and I won't discuss it in this document. Developing a trading strategy in AmiBroker, or any other software, means you need to embed the logic of order flow into your strategy. If you are long and want to Scaleout, you need to allow the sell signal trigger more than. Backtesting is one of the most important aspects of developing a trading. That's Ok newbietraderI'm sure there's plenty of people in the same situation as yourself - when you're just starting out, there's so much to learn, and you're itching to trade, as very dear old friend used to say "make haste slowly". Remaining features are much more easy to understand. There is nothing dismissive about that, it is is just common sense and most logical course of action. I will for sure take a online brokerage accounts for day trading is it good time to invest in stock market. Now with the SetOption function you can either supress report generation for backtests or enable report does coinbase have account numbers best site to buy bitcoin for dark web during certain optimization steps, all from code level.

You're asking a couple of different questions in the one post exrem and "entry bar volume has been hit xx times". It then rotationally invests in three stocks those with the highest rate of change that are in the same sector as the highest ranked ETF. And to answer your final question, Amibroker treats all scaling entries and exits as occurring within the same trade. It is accomplished by reconstructing, with historical data, trades that would have occurred in the past using rules defined by a given strategy. Monte Carlo Simulation Prepare yourself for difficult market conditions. Maximum loss stops work in a similar manner - they are executed when the low price for a given day drops below the stop level that can be given as a percentage or point increase from the buying price. Investopedia is part of the Dotdash publishing family. Now you can control dollar amount or percentage of portfolio that is invested into the trade. When the formula is correct AmiBroker starts analysing your symbols according to your trading rules and generates a list of simulated trades. One of the most useful things that you can do in the analysis window is to back-test your trading strategy on historical data. Make sure you have typed in the formula that contains at least buy and sell trading rules as shown above. Mea culpa. BTW: linking to existing material is very welcome as it makes it easier to find related posts.

Quantopian has very narrow scope of interest and narrower audience. Maximum loss stops work in a similar manner - they are executed when the low price for a given day drops below the stop level that can be given as a percentage or point increase from the buying price. Here is a list of the most important things to remember while backtesting:. Please note that writing many static variables into physical disk file takes time and it blocks all static variable access so you should AVOID specifying too small auto-save intervals. The AmiBroker code has been hand optimized and profiled to gain maximum speed and minimize size. And they should not be surprised if somebody points to existing material when we see something like "5 minute total forum read time". You mentioned the Clenow rotation thread. Third party services, blogs, courses, books, add-ons. By default stops are executed at price that you define as sell price array for long trades or cover price array for short trades. Initially the idea was to allow faster chart redraws through calculating AFL formula only for that part which is visible on the chart. You can set and retrieve the tick size also from AFL formula using TickSize reserved variable, for example:. In other words you can trade stocks on margin account. Useful when you want to narrow your analysis to certain set of symbols. What am I missing here?

And to answer your final question, Amibroker treats all scaling entries and exits as instant bitcoin buy no id coinbase verification error within the same trade. In the previous versions of AmiBroker, if you wanted to back-test system using both long and short trades, you could only simulate stop-and-reverse strategy. Also there were only 2 short signals for that particular bar so, the rest of the list shows long signals in order of position score Although this feature can be used independently, it is intended to be used in combination with MaxOpenLong and MaxOpenShort options. Note that these limits are independent from global limit MaxOpenPositions. Please note that we are using the same cross function but the opposite order of arguments. As ATR changes from investment apps like robinhood internationa massachusetts cannabis stock to trade - this will result in dynamic, volatility based stop level. After changing settings please remember to run your back testing again if you want the results to be in-sync with the settings. But now AmiBroker enables you to have separate trading rules for going long and for going short as shown in this simple example:. The ApplyStop function allows now to change the stop level from trade to trade.

The backtester assumes that price data follow tick size requirements and it does not change price arrays supplied by the user. This kind of stop is used to protect profits as it tracks your trade so each time a position value reaches a new high, the trailing stop is placed at a higher level. I use a different data feed and social trading risks forex sharp trading system Sector symbols are based on my data feed. Enjoy advanced editor with syntax highlighting, auto-complete, parameter call tips, code folding, auto-indenting and in-line error reporting. Use dozens of pre-written snippets that implement common coding tasks and patterns, or create your own snippets! I have another question regarding scale in arrows on the chart. The second screen is the actual backtesting results report. That is precisely the reason why newcomers may get dismissive comment. Initially the idea was to allow faster chart redraws through calculating AFL formula only for that part which is visible on the chart. They may be related, but look like different problems. Above is a great example of indicator based scalein. Here is a list of the most important things to remember while backtesting:. Backtesting is one of the most important aspects of developing a trading. This can give you valuable insight into strengths and weak points of your system before investing real money. If you want to see only single trade arrows opening and closing currently selected trade you should double click the line while holding SHIFT key pressed. Is it to use exrem first before scale-out or scale-out first after that do the exrem? Your response made perfect sense. Useful when you want to narrow your analysis to certain set of etrade mobile pro android download algo trading getting started.

Risk Management. Thanks in advance. The meaning and examples on using them are given later in this chapter. Personal Finance. CSV file of signals and then re-importing them and using that data as if it's a price series. These customizations include everything from time period to commission costs. If you don't define them AmiBroker works as in the old versions. Backtesting Definition Backtesting is a way to evaluate the effectiveness of a trading strategy by running the strategy against historical data to see how it would have fared. I honestly felt they were very worthwhile resources that would help a new user get a good start on coding rotational systems. If you for some reason want auto-saves when AmiBroker is running, then you can use this function. Please see below code This enables you to implement for example volatility-based stops very easily.

As you said, I think scale-in average up is better than scale-out take profit early or holding to position when price against my position hoping it will reverse in my case. What is correct way to combine them? From some preliminary analysis, I've found that, counterintuitively to me at least , it's best to invest in all sectors EXCEPT the highest ranking sector. Backtesting is one of the most important aspects of developing a trading system. By using Investopedia, you accept our. Anyways, that's my two cents. If default tick size is also set to zero it means that there is no minimum price move. And to answer your final question, Amibroker treats all scaling entries and exits as occurring within the same trade. CSV file of signals and then re-importing them and using that data as if it's a price series. Built-in stop types include maximum loss, profit target, trailing stop incl. Automated Forex Trading Automated forex trading is a method of trading foreign currencies with a computer program. For example in Japan - you can not have fractional parts of yen so you should define global ticksize to 1, so built-in stops exit trades at integer levels. To reproduce the example above you would need to add the following code to your automatic analysis formula:. I hope that we can start fresh. If you want to see only single trade arrows opening and closing currently selected trade you should double click the line while holding SHIFT key pressed down. Backtesting as you you seem to be doing is great, because it gives you a sense of how a strategy might perform, but getting it "wrong", or getting the logic out of sync, means that you end up fooling yourself.

So scaling doesn't impact your MaxOpenPositions count, only the initial entry and final exit alter the number of positions open. In this chapter we will consider very basic moving average cross over. Alternatively you can exchanges like coinbase aml bitcoin token exchange the type of display by selecting appropriate item from the context menu that appears when you click on the results pane with a right mouse button. Sets various options in automatic analysis settings. Dynamic Position Sizing. Hi newbietraderYou're asking a couple of different questions in the one post exrem and "entry bar volume has been hit xx times". So in the example above it uses ATR 10 value from the date of the entry. ChandelierN-bar timed all with customizable re-entry delay, activation delay and validity limit. I'm also trying to come up with a better ranking method than what Clenow uses. Here is a list of the most important things to remember while backtesting:. Less typing, quicker results Coding your formula has never been easier with ready-to-use Code snippets. Check worst-case scenarios and probability of ruin. Multiple data-source support You are not locked to one data anfuso backtesting gamma scalping backtest, you can connect to eSignal, IQFeed, Interactive Brokers, QCharts, among others Multi-page Real-Time quote window Real-time window has pages that allow you to switch quickly between various symbol lists. The AmiBroker code has been hand optimized and profiled to gain maximum speed and minimize size. The underlying theory is that any strategy that worked well in the past is likely to work well in the future, and conversely, any strategy that performed poorly in the past is likely to perform poorly in the future.

Again it is not about any particular person, just a pattern observed from time to time. Note however that turning it on gives huge performance penalty arithmetic operations are performed even 4x slower palladium tastytrade brokerage account for us expats this option is ON, so don't use it unless you really have to. A trading system with multiple scale in and scale out orders. To simulate this just enter 50 in the Account margin field see pic. AmiBroker checks for nulls that appear in the beginning of the arrayand in the end of the array and once non-null value is detected it assumes no further holes nulls in the middle. These arrays have the following names: buyprice, sellprice, shortprice and coverprice. By using Investopedia, you accept. To test if the close price crosses above exponential moving average we will use built-in cross function:. In today's world of bloatware we are proud to deliver probably the most compact technical analysis application. Check worst-case scenarios and probability of ruin. Until now we discussed investing in pot stocks australia when to sell stocks reddit simple use of the back tester. Please note that this settings sets the margin for entire account and it is NOT related to futures trading at all. This forum is much more diverse than Quantopian. Once I get some of these ideas working better and integrated into the strategy, I'll post it. The tone here is much different than it is at Quantopian for example, where there's a definite sense that people are collaborating, improving, and growing. Then, the plan is to see which combination of sectors perform the best e.

Multiple charts, indicators, drawing tools can be placed on user-definable layers that can be hidden or made visible with single click. Is it to increase the overall size of the profit? I think I was frustrated that I couldn't figure it out myself. I scoured this forum as well as other sources before deciding to post my question. There is a famous strategy by Larry Connors called TPS which employs this same approach maybe mradtke had a hand in its development? Yearly, quarterly, monthly, weekly and daily charts, Intraday charts, N-minute charts, N-second charts Pro version , N-tick charts Pro version , N-range bars, N-volume bars. For example, to back test on weekly bars instead of daily just click on the Settings button select Weekly from Periodicity combo box and click OK , then run your analysis by clicking Back test. You helped. What is correct way to combine them? Trading rules can use other symbols data - this allows creation of spread strategies , global market timing signals, pair trading, etc. For example I have equity I want to allocate for first trade but want to use only for first entry and when criteria meet for second entry I want to spend again. For example you can purchase fractional number of units of mutual fund, but you can not purchase fractional number of shares.

The close identifier refers to built-in array holding closing prices of currently analysed symbol. The debugger allows you to single-step crypto exchange for nyc can i buy bitcoin with capital one your code and watch the variables in run-time to better understand what your formula is doing. But now AmiBroker enables you to have separate trading rules for going long and for going short as shown in this simple example:. Once you have your own rules for trading you should write them as buy and sell rules in AmiBroker Formula Lanugage plus short and cover if rockport day trading twin gore slip on leading indicators want to test also short trading. On AmiBroker forum we've got huge diversity. Calling function with interval set to zero disables auto-save. Scale in as percent of allocated equity AFL Programming. All these settings could be changed by the user using settings window. I assume that you are testing against a watch list that is large enough that you may not be able to take all entries on a given day.

Just the opposite. Thank you for the great advice, sinecospi. First you need to have objective or mechanical rules to enter and exit the market. To simulate this just enter 50 in the Account margin field see pic. In my case, I've spent a lot of time on this forum -and greatly appreciate that we have it since it's so much easier to use than the old Yahoo group -but that's not reflected in my "read time' since I only registered in order to finally ask for help on something that had been dogging me for weeks. After testing scale-out, it seems that the performance worst than without scale out. The following table shows the names of reserved variables used by Automatic Analyser. Note2: old backtester Equity function ignores settlement delay StaticVarAutoSave - allow periodical auto-saving of persistent static variables in addition to saving on exit, which is always done. Risk management occurs anytime an investor or fund manager analyzes and attempts to quantify the potential for losses in an investment. You can set and retrieve the tick size also from AFL formula using TickSize reserved variable, for example:. Take insight into statistical properties of your trading system. I haven't yet but I'll let you know if I do. As you can see in the picture above, new settings for profit target stops are available in the system test settings window. PS I am pretty sure Howard Bandy has coded a version of your system and of course many other systems in his 2nd book "Quantitative Trading Systems" which is also a great place for a newbie to grow his AmiBroker skills. This will give you raw or unfiltered signals for every bar when buy and sell conditions are met. First entry criteria is 4 period rsi less than 25, sclae in 2nd entry when 4 period rsi is less then Calling function with interval set to zero disables auto-save. The debugger allows you to single-step thru your code and watch the variables in run-time to better understand what your formula is doing. Enjoy advanced editor with syntax highlighting, auto-complete, parameter call tips, code folding, auto-indenting and in-line error reporting. Concise language means less work Your trading systems and indicators written in AFL will take less typing and less space than in other languages because many typical tasks in AFL are just single-liners.

Do some research on stop losses - how to use them depends on your strategy, and the reason for using them. The down side of the Phase 1 approach is that you have to assume that the first entry signal is the one that will actually be taken in the back test. If you're going to use trade delays, then I believe you will need to adjust your position size array as well, with something like:. Why do you want to increase the number of trades? I re-read your original post and lo-and-behold I had not read it carefully enough the first time. I've found that it's one of the best ways of minimizing drawdown. In today's world of bloatware we are proud to deliver probably the most compact technical analysis application. It was because buy and sell reserved variables were used for both types of trades. First entry criteria is 4 period rsi less than 25, sclae in 2nd entry when 4 period rsi is less then Thank you for the help, it's much appreciated. You can however code your own kind of stops and exits using looping code. It also allows to create custom metrics, implement Monte-Carlo driven optimization and whatever you can dream about. Scale Trading with AmiBroker. Optimization engine supports all portfolio backtester features listed above and allows to find the best performing parameters combination according to user-defined objective function optimization target Exhaustive or Smart Optimization You can choose Exhaustive full-grid optimization as well as Artificial Intelligence evolutionary optimization algorithms like PSO Particle Swarm Optimization and CMA-ES Covariance Matrix Adaptation Evolutionary Strategy that allow upto optimization parameters to be used.